[ad_1]

I must confess that when I started these updates in February, I did not expect to be doing them in July, but a crisis is as good a time as any, to learn new lessons and relearn old ones. As the virus makes a comeback, particularly in the United States, it is not surprising that markets reflect the uncertainty that we all feel about how the rest of the year will play out in both our personal and business lives, with mood rising and falling on positive and negative news stories. In this post, I will begin by updating the numbers for markets overall, and within the equity market, across regions, sectors and industries. I will then use the differences I see across companies to highlight flexibility in investing, operating, financing and cash return policies as the one quality that seems to be separating the winners from the losers in these last few months, and argue that this represents an acceleration of a longer-term shift towards more nimble and adaptable business models.

Market Update

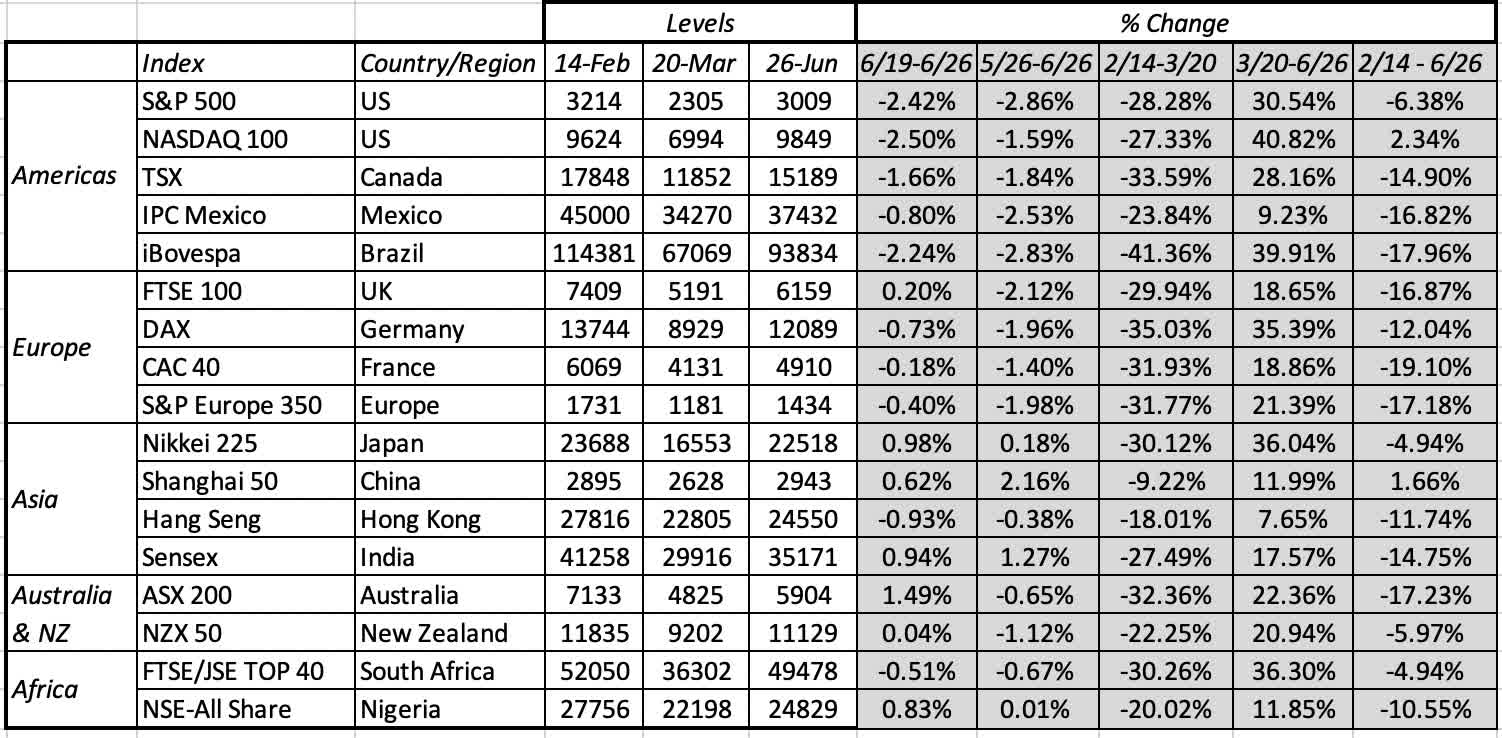

If you have been reading all of my viral market updates during this crisis, I admire your fortitude, and I know that you will get a sense of deja vu, as you read this section, since I follow the same road map on each of them. I start, as always, by looking at US dollar returns on selected equity indices around the world:

Looking at the entire time period (2/14-6/26), US equity indices have done better than European equity indices, with a strong rebound from the lows of March 20 allowing for a complete recoupment of losses in the NASDAQ and an almost complete retracing for the S&P 500. Asian equities have diverged, with Japan and China performing better than India. As equities have seesawed, US treasury bonds have stabilized, after a steep drop in yields in the first four weeks of the crisis:

The treasury rates have settled in, at least for the moment, at close to zero at the short end of the maturity spectrum and at about 0.65-0.75% for the 10-year bonds and 1.2-1.4% for 30-year bonds. I know that there is a widely held view that it is the Fed that has engineered the rate drop, but note that much of the decline occurred before the Fed made its quantitative easing announcements in mid-March. I think that the Fed’s real impact has been on private lending, with its March 23rd announcement that it would operate as a backstop in corporate bond and lending markets. You can see the effects of that announcement on default spreads for corporate bonds, across ratings classes:

Note the climb in default spreads between February 14 and March 23, with investment grade (BBB) rated bonds almost tripling during that period, and the pull back in spreads since, to end at levels higher than on February 14, but well below the March 23rd levels. Mirroring the changes in the price of risk in the corporate bond markets, the price of risk in equity markets (measured with an implied…

[ad_2]

Read More: A Viral Market Update XI: The Flexibility Premium